Every year, CPA/PFS professionals walk past an unusually powerful business-development advantage hiding in plain sight: tax season.

Tax preparation creates a moment of maximum financial visibility and maximum trust density. And, for many firms, that combination happens only once a year at scale.

Most CPA firms that offer investment advisory services already know that only a minority of tax clients are also investment advisory clients. However, most are at a loss to answer this key question: “What can we do during tax season that is truly client-centered, demonstrably objective, and operationally feasible, to secure new investment advisory clients from our much larger tax preparation client base?”

One compelling answer is to use the data you already see (brokerage statements, fund/ETF line items) to run a rapid, transparent comparative analysis of the client’s mutual funds and ETFs, right when the client is already thinking seriously about their financial life.

Later in this article, we describe a new way to do this that you could find to be a true gamechanger, making it possible to rapidly grow your investment advisory client base in a single tax season.

Why tax season changes the recruiting math for CPA/PFS advisors

1) You’re already inside the trust moat. Traditional investment advisors spend years trying to earn what a CPA often has already earned: credibility grounded in accuracy, confidentiality, and long-term relationship. That trust dramatically lowers the friction of “Can we take a deeper look at this?”

2) You have immediate access to holdings data. Tax prep frequently surfaces brokerage statements that reveal the investments the client owns (and often how concentrated they are). That creates a natural opening for a disciplined, client-friendly question:

“Would it be useful if we did an objective check on how these holdings have compared to other options in the same asset classes, using the performance factors that matter most to you?”

3) Clients are mentally in “review mode.” They’re gathering documents, revisiting income/withholding, seeing capital gains, and confronting reality. That’s the right psychological context for an evidence-based review; not a pitch.

The real opportunity: making “performance gaps” visible in minutes

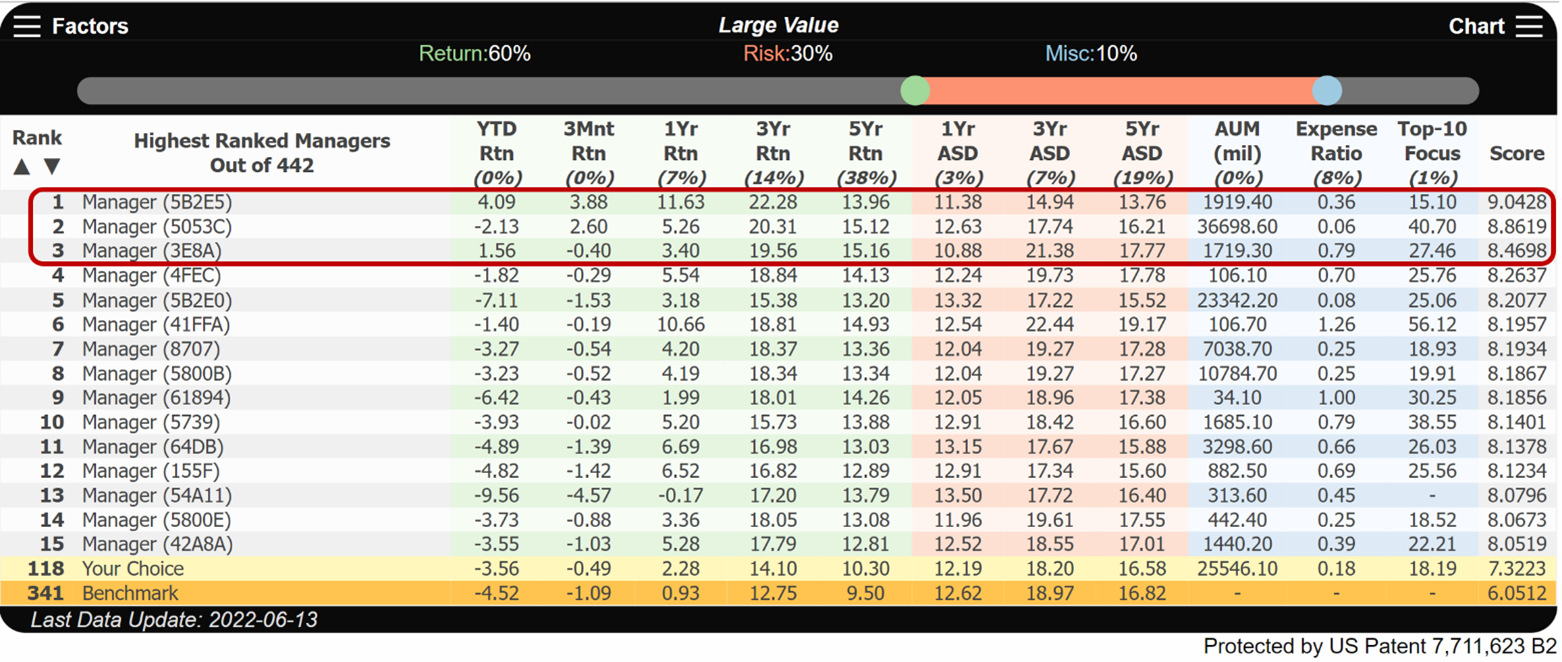

The ProRapidReview approach to new investment client recruitment is built around a simple idea: within a given asset class, you should be able to score and rank hundreds of mutual fund and ETF options using a custom-weighted blend of objective quantitative performance factors; not just a single return period or.

This process provides you with the ability to provide the client with an answer to this key question: “How did my mutual funds and ETFs do compared to all of the alternatives I could have selected?” and not just a comparison to a single benchmark index.

The often-large performance gaps that will be revealed and the objectivity and transparency of the process – something the client will have never before experienced – provides a you will a compelling competitive advantage.

Mechanically, the workflow is:

- Enter a mutual fund and/or ETF (ticker or name).

- The tool identifies the relevant asset class and runs an initial comparison using default return + volatility weightings.

- You (and the client, if appropriate) adjust which metrics matter and how heavily they’re weighted; pulling from a menu of 48 quantitative factors (returns across multiple periods, volatility measures, Sharpe/Sortino/Treynor, fees/expense ratio, manager tenure, turnover rate, alpha, downside deviation, and more).

- The tool produces a composite score and rank order, plus a chart visualization designed to highlight how few choices tend to separate from the “slope of mediocrity.”

This matters in practice because it reframes the conversation from “Trust my opinion” to “Do you want an objective process that helps us both see the tradeoffs clearly?”

That’s a qualitatively different client experience.

A CPA/PFS tax-season playbook that doesn’t wreck your workflow

Here’s a practical, low-disruption model that respects tax season constraints.

Step 1: Create a “portfolio checkup” lane (separate from tax prep)

Offer a simple option:

- Tax meeting remains tax.

- Checkup is a separate, optional, scheduled review (15–25 minutes) that can happen:

- after the return is filed, or

- in a dedicated slot during the season for higher-value clients.

This separation is important for professionalism, client comfort, and compliance hygiene.

Step 2: Triage clients (don’t boil the ocean)

Pick criteria that match your business model, such as:

- taxable brokerage assets above a threshold

- self-directed investors with messy holdings

- high concentration in a few funds

- clients paying high advisory fees elsewhere

- clients with repeated taxable distributions / avoidable tax drag (a frequent “pain signal”)

Step 3: Run a 3-holding “first look”

During the checkup meeting, focus on the client’s top 3 holdings (by dollars or importance). This keeps the meeting crisp while still delivering a strong signal.

Use the tool to:

- show the default return/risk framing

- then ask the client which factors matter (fees, downside protection, consistency, etc.)

- produce the ranking and compare the client’s holding to top-ranked alternatives within the same asset class

The goal is not to “win the argument.” The goal is to help the client see that there may be meaningful differences between what they own and what else has historically met their objectives more effectively.

Step 4: Convert the insight into a next step

A clean close is not aggressive. It’s operational:

- “If you’d like, we can do this across your full portfolio, identify and analyze comparative performance gaps, document the rationales for portfolio adjustments, and build an ongoing monitoring cadence.”

That’s a fiduciary-aligned offer, not a sales line.

Why this can be a compliance asset, not a liability

When investment selection becomes a defendable process (factors → weights → score → ranking → documented rationale), you’re not just improving outcomes; you’re improving governance.

The ProRRTSM explicitly positions you with a way to provably demonstrate alignment with “best interest” expectations and requirements, to both clients and regulators, by showing that recommendations match client objectives and reduce conflicts.

Start with the free “Checkup” version; on purpose

The ProRRTSM offers a free Checkup tier that retains the core functionality but limits investment-name visibility; useful for screening current recommendations and demonstrating the process before you commit to a subscription.

This is especially relevant for CPA/PFS advisors because it lets you validate two things quickly:

- Client value: Do clients respond to this kind of transparency?

- Firm ROI: Does it reliably create productive advisory conversations with the right people?

A final note on tone: the best version of this is calm

The highest-performing version of this strategy is not “gotcha.” It’s not “your advisor is terrible.”

It’s a quiet, professional reveal:

- “Here’s how your holdings compare within their peer set.”

- “Here’s what your stated priorities imply.”

- “Here’s what rises to the top when we measure usomg your investment preferences consistently.”

That is exactly the kind of client experience CPA/PFS professionals should own.

And tax season is when you can do it at scale.

See how it works here. And try it for free here.

Eric S. Smith, J.D.

Eric S. Smith, J.D. is CEO of Decision Technologies Corporation, and President and Investment Advisor Representative of Trustee Empowerment & Protection, Inc., a Registered Investment Advisor